All portable, LMT, industrial, SLI and EV batteries made available on the Belgian market must be declared to Bebat. This applies to both batteries sold separately (replacement market) and built-in and supplied batteries (initial installation), as well as both non-rechargeable (primary) and rechargeable batteries.

Only batteries intended for equipment used in space and batteries exclusively for military purposes are an exception.

The five categories are:

- Portable batteries ≤ 5 kg: these are everyday household batteries, such as those found in watches, remote controls, laptops, etc.

- Light vehicle batteries (LMT) ≤ 25 kg: these are batteries specifically designed to power small electric vehicles such as e-bikes, e-scooters, e-mopeds, etc.

- Industrial batteries: these are batteries specifically designed for professional or industrial applications – regardless of weight. Batteries designed for energy storage (ESS) are also considered industrial. A battery weighing more than 5 kg that is not an EV, SLI or LMT battery is always considered an industrial battery.

- Starting, lighting and ignition (SLI) batteries: these are all batteries specifically designed for starting, lighting or ignition purposes and which may also be used for auxiliary or reserve functions in vehicles, other means of transport or machinery.

- Electric vehicle (EV) batteries: any traction battery used to power a hybrid or electric vehicle of category L (> 25 kg) or categories M, N & O.

Important: certain battery types can not be put on the market:

- From 18/02/2024: Portable batteries containing more than 0.02 weight percentage of cadmium (expressed in metallic cadmium), regardless of whether sold separately or in devices or whether built into light means of transport or other vehicles.

- From 18/08/2024: Portable batteries containing more than 0.01 weight percentage of lead (expressed in metallic lead), regardless of whether they are built into devices.

- From 18/08/2028: Portable zinc button cell batteries containing more than 0.01 weight percentage of lead (expressed in metallic lead), regardless of whether they are built into devices.

An overview of all legislation relating to this can be found at https://www.bebat.be/en/b2b/legislation.

Do I have to submit a declaration to Bebat?

The principle is that the first party to make batteries available on the Belgian market must be the party that reports it. Therefore, the answer to whether you must declare batteries depends on:

-

Where your business is based

-

Where you purchase the batteries

-

Whether you use the batteries for your own use or sell them

-

Where you sell the batteries

You can find all the information about who is responsible for reporting, which batteries you need to report, and how to make this report here: https://www.bebat.be/en/producing-importing/declarations.

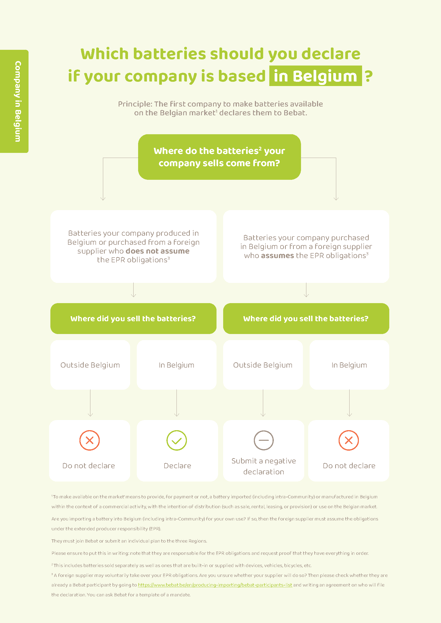

Your company is located in Belgium

Which batteries do you need to declare if your company is located in Belgium? See the diagram below:

In other words, batteries that meet the following criteria:

- Produced by your company in Belgium or purchased from a foreign supplier that does not take over your declaration obligation;

- Sold in Belgium;

- Separate or built into a device.

How can you be certain whether your foreign supplier is taking over your take-back obligation?

A foreign supplier may voluntarily take over your EPR obligations.

First check whether they are already a Bebat participant at https://www.bebat.be/en/producing-importing/bebat-participants-list and set out in writing (via a mandate) who will submit the declaration.

Your declaration can be based on sales data or purchase data.

- Declaration based on sales data:

If you only work with invoices when selling batteries (separately or built-in/provided), you may base your declaration on your sales data. - Declaration based on purchase data:

If you only work with receipts or a combination of receipts and invoices, your declaration must be based on your purchase data.

Consider the following when determining which batteries to declare.

Declaration based on sales data

This type of declaration applies if you only work with invoices when selling batteries (separately or built-in/provided).

To be included in the declaration

- Batteries you have purchased in Belgium or that are produced by your company and/or purchased from a foreign supplier that does not take over your declaration obligation.

To be deducted from the declaration

- Batteries you have sold abroad and purchased in Belgium.

- Batteries you have sold abroad and purchased abroad from suppliers that take over your declaration obligation at Bebat.

Do not need to be declared

- Batteries you have sold or purchased in Belgium.

- Batteries you have sold abroad and have produced in Belgium or that are purchased abroad from suppliers that do not take over your declaration

Declaration based on purchase data

This type of declaration applies if you only work with receipts (whether or not combined with invoices) when selling batteries (separately or built-in/provided).

To be included in the declaration

- Batteries you have purchased abroad from suppliers that do not take over your declaration obligation at Bebat or that you have produced in Belgium.

To be deducted from the declaration

- Batteries you have purchased in Belgium and sold abroad.

- Batteries you have purchased abroad from suppliers that have taken over your declaration obligation at Bebat and that you sell abroad.

- Batteries you have purchased abroad from suppliers that do not take over your declaration obligation at Bebat or that you have produced in Belgium and sold abroad on the condition that you included these batteries in your declaration on purchase or production.

Do not need to be declared

- Batteries purchased in Belgium and sold in Belgium.

- Batteries you have purchased abroad from suppliers that do not take over your take-back obligation at Bebat or that you have produced in Belgium and sold abroad on the condition that you did not include these batteries in your declaration on purchase or production.

- Batteries purchased abroad for personal use. These must be declared by the foreign supplier.

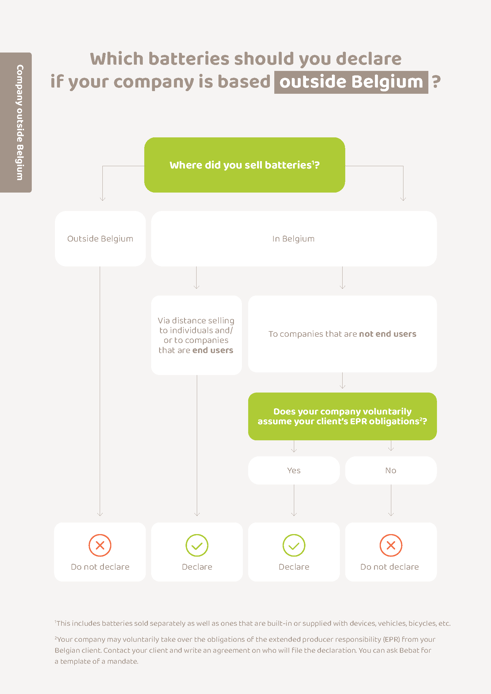

Your company is located outside of Belgium

Which batteries do you need to declare if your company is located outside of Belgium? See the diagram below:

Batteries that meet the following conditions must therefore be declared:

-

Sold by your company (by distance selling) to Belgian private individuals and/or businesses that are end-users

-

Sold by your company to Belgian businesses that are not end-users, but for which you voluntarily assume the WEEE obligations.

- Sold separately or built into a device.

Your declaration is based on your sales data as described above.

Nothing to declare? Submit a zero declaration.

Do you not have anything to declare for a specific period? Submit a zero declaration.